Understanding How to Compute a U.S. shareholder’s GILTI inclusion was published by JD Supra on 2/27/19.

The Tax Cuts and Jobs Act added section 951A to the Internal Revenue Code. This new section requires a U.S. shareholder of a Controlled Foreign Corporation (CFC) to

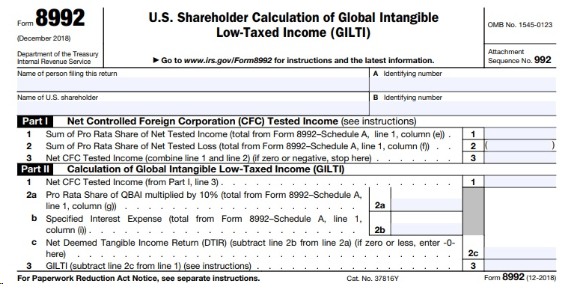

include in gross income the shareholder’s Global Intangible Low-Taxed Income (GILTI) for years in which they are a U.S. shareholder of a CFC for tax years of the CFC beginning after 2017. IRS Form 8992 (U.S. Shareholder Calculation of Global Intangible Low-Taxed Income (GILTI) together with its Schedule A is used to compute a U.S. shareholder’s GILTI inclusion (U.S. Shareholder Calculation of GILTI).

What is a CFC?

A CFC is a foreign corporation that has U.S. shareholders that own (directly, indirectly, or constructively) on any day of the tax year of the foreign corporation, more than 50% of:

- The total combined voting power of all classes of its voting stock; or

- The total value of the stock of the corporation.

Who is a U.S. Shareholder?

A U.S. shareholder is a U.S. person who owns (directly, indirectly, or constructively):

- 10% or more of the total combined voting power of all the classes of voting stock of a CFC or

- 10% or more of the total value of shares of all classes of stock of a CFC.

Who has to file Form 8992 and Schedule A?

Any U.S. shareholder of one or more CFCs that must take into account its pro rata share of the tested income or tested loss of the CFC(s) in determining the U.S. shareholder’s GILTI inclusion, if any, under section 951A.

Here are Definitions need for completion of Schedule A in Form 8992:

A. What is Tested Income?

“Tested Income” (with respect to any CFC for any taxable year of such CFC), is the EXCESS (if any) of:

- the gross income of such corporation

- any item of income

- any gross income taken into account in determining the subpart F income of such corporation,

- any gross income excluded from the foreign base company income and the insurance income of such corporation

- any dividend received from a related person,

- any foreign oil and gas extraction income

Over

- the deductions (including taxes) properly allocable to such gross income

B. What is Tested Loss?

“Tested Loss” (with respect to any CFC for any taxable year of such CFC), is the EXCESS (if any) of:

- the deductions (including taxes) properly allocable to such gross income

Over

- the gross income of such corporation

C. What is Net CFC Tested Income?

“Net CFC Tested Income” (with respect to any CFC for any taxable year of such CFC), is the EXCESS (if any) of:

(A) the aggregate of such shareholder’s pro rata share of the tested income of each CFC with respect to which such shareholder is a U.S. shareholder for such taxable year of such U.S. shareholder (determined for each taxable year of such CFC which ends in or with such taxable year of such U.S. shareholder)

Over

(B) the aggregate of such shareholder’s pro rata share of the tested loss of each CFC with respect to which such shareholder is a U.S shareholder for such taxable year of such U.S. shareholder (determined for each taxable year of such CFC which ends in or with such taxable year of such U.S. shareholder)

D. What is a Qualified Business Asset Investment (QBAI)?

QBAI is the average of the CFC’s aggregate adjusted bases, as of the close of each quarter of its taxable year, in specified tangible property used in its trade or business in the production of tested income, and for which a deduction is allowable under section 167.

Section 167 of the Internal Revenue addresses Depreciation. There shall be allowed as a depreciation deduction a reasonable allowance for the exhaustion, wear and tear (including a reasonable allowance for obsolescence):

(1) of property used in the trade or business, or

(2) of property held for the production of income

QBAI is derived from Form 5471 (Information Return of U.S Person with Respect to Certain Foreign Corporations).

E. What is Specified Interest Expense?

The amount of interest expense taken into account under section 951 in determining the net CFC tested income for the tax year to the extent the interest income attributable to that expense is not taken into account in determining the net CFC tested income.

Putting it all together: Form 8992 and Schedule A

Calculations are set forth as follows on Page 2 of Form 8992:

Don’t be a Victim of your Own Making

The GILTI Regime is complex. Tax Forms 8992 and 5471 work in tandem. It is recommended that Taxpayers seek the assistance of a specialized Tax Advisor for the accurate completion of Form 8992.

https://www.jdsupra.com/legalnews/understanding-how-to-compute-a-u-s-72734/