Taxpayers who engaged virtual currency transactions in 2020 must answer a Yes or No Question on page 1 of Form 1040 or Form 1040-SR. The question is: “At any time during 2020, did you receive, sell, send, exchange or otherwise acquire any financial interest in any virtual currency? Failing to answer will prevent electronic filing of a 2020 Form 1040 or Form 1040-SR. This question first appeared in Schedule 1 of the 2019 Form 1040. Moving the Question from Schedule 1 of the 2019 Form 1040 to the first page of Form 1040 and 1040-SR in 2020 is an IRS enforcement escalation.

Because IRS classifies virtual currency as an asset, If the answer is Yes, its disposal in an investment sales transaction requires reporting the transaction on Form 8949.

Taxpayers that received virtual currency as compensation for services or disposed of any virtual currency held for sale to customers in a trade or business must report the income the same way they would report other income of the same type (for example, W-2 wages on Form 1040 or 1040-SR, line 1, or inventory or services from Schedule C on Schedule.

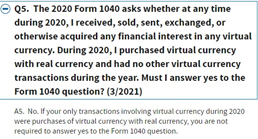

If Taxpayers that have not engaged in any disposal transaction involving virtual currency, just check the “No” box.

A transaction involving virtual currency includes:

- The receipt or transfer of virtual currency for free (without providing any consideration). including from an airdrop or hard fork.

- An exchange of virtual currency for goods or services.

- A sale of virtual currency.

- An exchange of virtual currency for other property, including for another virtual currency; and

- A disposition of a financial interest in virtual currency.

Transaction that do not affect taxable income are:

- Buying virtual currency with dollars and just holding on to it

- Sending virtual currency to a different virtual currency wallet under the same account owner

“A transaction involving virtual currency does not include the holding of virtual currency in a wallet or account, or the transfer of virtual currency from one wallet or account you own or control to another that you own or control”.

Taxpayers received further clarity when the IRS updated its Virtual Currency FAQ’s in March 2021

Taxpayers ought to gather documents and organize tax records

The Internal Revenue Code and regulations require Taxpayers to maintain records that support the information provided on tax returns. Taxpayers should maintain records documenting receipts, sales, exchanges or other dispositions of virtual currency and the fair market value of the virtual currency.

Virtual Currency is a priority for the IRS

IRS has stated that Taxpayers need to understand their obligations involving virtual currency. IRS will take steps to ensure fair enforcement of the tax laws for those who do not follow the rules involving virtual currency.

Consult your specialized tax advisor. ©