U.S. Taxpayers (includes a citizen, permanent resident, corporation, partnership, limited liability company, trust and estate) are required to file a Report of Foreign Bank and Financial Accounts (FBAR) if they have:

- a financial interest in or signature or other authority over at least one financial account located outside the United States, AND

- the aggregate value of those foreign financial accounts exceeded $10,000 at any time during the calendar year reported.

The Bank Secrecy Act (BSA) requires U.S. Taxpayers to report certain foreign financial accounts to the U.S. Treasury Department and retain certain related records of those accounts.

There are Penalties for failure to file an FBAR

U.S. Taxpayers could be subjected to civil monetary penalties and/or criminal penalties for FBAR reporting and/or recordkeeping failures. Assertion of penalties depends on related facts and circumstances. The IRS states in the “IRS FBAR REFERENCE GUIDE” that “the largest civil penalty for a willful violation of the FBAR requirements is the greater of $124,588 or 50 percent of the balance in the account at the time of the violation. Non-willful violations can result in a penalty as high as $12,459 for each violation. Criminal violations of FBAR rules can result in a fine and/or five years in prison”.

The Jane Boyd Case: is it per account or per violation?

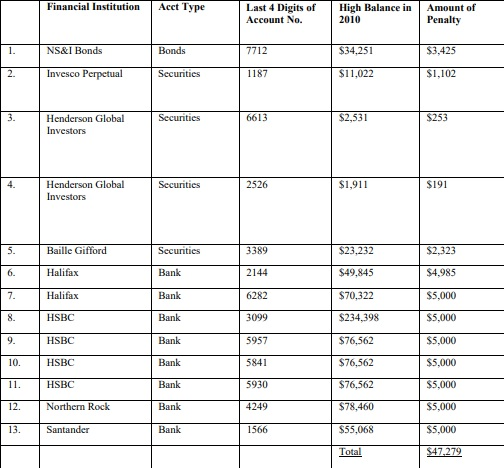

Jane Boyd is a U.S. Person (U.S.A. v. Jane Boyd, Case No. CV 18-803-MWF (JEMx)) that during 2010 had a financial interest in, signatory authority over, and/or otherwise controlled 13 financial accounts in the United Kingdom with collective balances in excess of $10,000. (Id. No. 6). Mrs. Boyd did not report the interest and dividends on her 2010 federal income tax return, and the existence of her U.K. accounts on her U.S. tax return. Mrs. Boyd was required by BSA regulations to file an FBAR form disclosing the subject thirteen (13) accounts for 2010 but failed to timely do so. The IRS concluded that although Mrs. Boyd had committed thirteen FBAR violations, she had not willfully violated her reporting requirements and that she was eligible to mitigate the FBAR penalties since each account contained less than $250,000. On June 9, 2016, the IRS assessed the following penalties against Mrs. Boyd:

On June 10, 2016, the IRS sent Boyd a letter demanding payment of the FBAR penalties.

Mrs. Boyd wanted to pay $10,000, not $47,279

Both Mrs. Boyd and the U.S.A. did not dispute the facts giving rise to the 2010 FBAR penalty assessment against Mrs. Boyd. However:

• The Government argued that the statutory maximum penalty of $10,000 under 31 U.S.C. § 5321(a)(5)(B) for non-willful violations relates to EACH foreign financial account.

• Mrs. Boyd contended that if there is a non-willful failure to file an FBAR, the penalty cannot exceed $10,000, regardless of the number of bank accounts required to have been listed on the FBAR.

Mrs. Boyd is not correct – the IRS Examiner has discretion

On May 13, 2015, the U.S. Department of the Treasury issued Interim Guidance for Report of Foreign Bank and Financial Accounts (FBAR) Penalties. The purpose of the Guidance was to implement procedures to improve the administration of the Service’s FBAR compliance program.

The Guidance states: “For most cases involving multiple non-willful violations, examiners will recommend one penalty for each open year, regardless of the number of unreported foreign financial accounts. In those cases, the penalty for each year will be determined based on the aggregate balance of all unreported foreign financial accounts, and the penalty for each year will be limited to $10,000”.

The Guidance ALSO STATES: “For other cases, the facts and circumstances (considering the conduct of the person required to file and the aggregate balance of the unreported foreign financial accounts) may indicate that asserting a separate non willful penalty for each unreported foreign financial account, and for each year, is warranted”.

Section 4.26.16.6.7 of the Internal Revenue Manual outlines IRS Examiner Discretion for assessing FBAR Penalties. Consequently, FBAR Penalty Amounts are in the “Best Judgement” of an IRS Examiner.

The Court’s Decision

Section 5321 of Title 31, (31 USC 5321) states that: “Civil penalties, provides overall civil penalty provisions for violations of the BSA and for violations of certain related statutes. It provides authority for assessing penalties when regulations for those penalties have not been issued. The penalties apply to violations of the BSA itself, the regulations under the BSA, or any geographic targeting or special measures order issued by Treasury, as well as penalties for taking certain actions, such as structuring, with the intent to evade BSA reporting or recordkeeping requirements”.

In the Jane Boyd Case, the Court stated that: “In light of the prominence of “transactions” and “accounts” in the language of section 5321, the Court determines that the statute contemplates that the relationship with each foreign financial account constitutes the non-willful FBAR violation. Because the Court determines that more than one FBAR violation may be assessed per year, the Court need not address Defendant’s additional argument that the IRS is bound to follow the mitigation guidelines set forth in the IRM”.

What this means is that the court viewed its interpretation of Section 5321 as one that in which a violation could be imposed on an individual account basis and not a “per one form” (multiple accounts in one form) basis; i.e., that each unreported foreign financial account could bear a $10,000 penalty. Consequently, the non-willful FBAR penalty was not limited to $10,000 per year.

Don’t be a Victim of your Own Making

The Report of Foreign Bank and Financial Accounts (FBAR) is not a tax form. Its filing is not required by the Internal Revenue Code. It is required by Title 31 of the Code of Federal Regulations. Title 31 is the Bank Secrecy Act (BSA). FBAR reporting is within the jurisdiction of the Financial Crimes Enforcement Network – a Bureau of the US Department of the Treasury – (FinCEN), (it is E-filed on FinCEN Form 114). However, the investigation and enforcement of FBAR filing requirements has been relegated from FinCEN to IRS (4.26.16.2.2); whereby IRS has the authority to enforce the provisions of Title 31: “31 CFR 1010.810(g) references a Memorandum of Agreement between FinCEN and the IRS, which redelegates FinCEN’s authority to enforce the provisions of 31 USC 5314 and 31 CFR 1010.350 and 1010.420 to the IRS”.

Mrs. Boyd tried to use as her defense argument that if Congress intended to impose a penalty based on each bank account required to be shown on the FBAR, Congress could have easily included such explicit language. It did not do so, rather the U.S. Treasury published guidelines giving IRS Examiners expanded discretion as per Internal Revenue Manual section 4.26.16.

Taxpayers with undisclosed foreign accounts ought to work with Tax Practitioners that understand FBAR penalties and are able to work with an IRS examining agent in order to achieve the best result for the Taxpayer.